D-Mart is a one-stop supermarket chain that aims to offer customers a wide range of basic home and personal products under one roof.

Each DMart store stocks home utility products – including food, toiletries, beauty products, garments, kitchenware, bed and bath linen, home appliances and more – available at competitive prices that our customers appreciate.

Core objective is to offer customers good products at great value.

DMart was started by Mr. Radhakishan Damani and his family to address the growing needs of the Indian family.

The launch of its first store in Powai in 2002,

DMart today has a well-established presence in 206 locations across Maharashtra, Gujarat, Andhra Pradesh, Madhya Pradesh, Karnataka, Telangana, Chhattisgarh, NCR, Tamil Nadu, Punjab and Rajasthan.

With our mission to be the lowest priced retailer in the regions we operate, our business continues to grow with new locations planned in more cities.

Business Structure:

D-Mart Hyper market One stop solutions & deals with 3-categories

- Food Items – 51.25% Revenue share.

- Groceries, Diary, Fruit & Vegetable, Frozen food, Snacks, Beverages and Confectionery..Etc.

- Non Food Items – 20.46% Revenue share.

- Home Care, Personal Care, Toiletries…etc.

- General Merchandise & Apparel – 28.29 % Revenue Share.

- Home Appliances, Plastic Goods, Crockery, Bed and bath products, Apparel, Foot Wear, Toys & Games….Etc.

Business Model: B2C

Buy Product from Manufacturers and sell to the End User.

That’s why operating profit Margin will be more.t

Benefits of Organized Retails Store:

- Visibility of Customer will be more, it increases the purchasing power of the customer.

- Product range is more in one place.

- Supplier gives more discount on bulk purchasing. Due to this selling price will be low.

Business Growth Parameters:

- Form of Business Type: Structural

| Mar-12 | Mar-13 | Mar-14 | Mar-15 | Mar-16 | Mar-17 | Mar-18 | Mar-19 | |

| Sales + | 2,209 | 3,341 | 4,686 | 6,439 | 8,584 | 11,898 | 15,033 | 20,005 |

| Expenses + | 2,071 | 3,126 | 4,345 | 5,981 | 7,920 | 10,929 | 13,680 | 18,371 |

| Operating Profit | 138 | 215 | 342 | 458 | 664 | 968 | 1,353 | 1,633 |

| OPM % | 6% | 6% | 7% | 7% | 8% | 8% | 9% | 8% |

2. Stage of Business: Growing

3. Evolution of Business: Geographical Expansion.

•Maharashtra (70)

• Gujarat (34)

• Telangana (21)

• Karnataka (16)

• Andhra Pradesh (11)

• Madhya Pradesh (6)

• Rajasthan (5)

• Punjab (3)

• Tamil Nadu (3)

• Chhattisgarh (3)

• NCR (1)

• Daman (1)

Now huge opportunity in North India, Central and east India.

2002 – 1 Store in Mumbai

2009-2010 – 25 store

2011-2012 – 50 Store

2015-2016 – 100 store

2019-2020 – 196 store

Industry Overview?

- India is a consumption-led economy with private consumption constituting ~60% to the GDP.

- Organized retail is expected to grow at ~1.6x the overall retail market.

- South and west account for ~57% of the total retail consumption.

- E-retail to clock 28-33% growth in medium term.

- Organized food and grocery retail, Past Year 2016-2019, Growth was 26%.

- Organized food and grocery retail is expected to grow at a highest CAGR of ~28-30% as compared to other segments yy 2019-2022.

- Organized food and grocery retail penetration is huge, because only 4 % growth shows in this sector.

Risk Factor:

- Discount price, how long they will survive due to more competition in the retails sector.

- Consequently 2 years getting lost in E-Commerce. What will be the future in E-Commerce?

The Key Product Categories Can Be Classified Into:

| Foods | Non-Foods | General Merchandise & Apparel |

| Dairy, staples, groceries, snacks, frozen products, processed foods, beverages & confectionery and fruits & vegetables | Home care products, personal care products, toiletries and other over-the-counter products | Bed & bath, toys & games, crockery, plastic goods, garments, footwear, utensils and home appliances |

| 51.25% Revenue Contribution FY 2018-19 | 20.46% Revenue Contribution FY 2018-19 | 28.29% Revenue Contribution FY 2018-19 |

| 51.55% Revenue Contribution FY 2017-18 | 20.03% Revenue Contribution FY 2017-18 | 28.42% Revenue Contribution FY 2017-18 |

| 53.32% Revenue Contribution 2016-17 | 19.85% Revenue Contribution 2016-17 | 26.83% Revenue Contribution 2016-17 |

Summaries of Qualitative Analysis:

- Company:

- Deals in the grocery, FMCG and Non-food retails sectors. Now a days organized retails is booming. The main point of attraction for customers are very cheap price as compared to other retailers.

- Everyday Low Cost, Everyday Low Price’ model to attract more customers. Also best quality maintained.

- Business Model: – B 2 C

- Form of Business – Structure.

- Stage of Business – Growth

- Evolution of Business – Geographic Expansion

The Company has 3- segment:

- Food items- Revenue sharing- 51.25%

- Non-Foods – Revenue —- – 20.46%

- General & Apparel – Revenue- – 28.29%

- In India still have more penetration space for groceries sectors.

- They work on revers logistic so that reduce the cost of transport.

- The new stores in the same markets reach absolute high revenue immediately, within three months, six months or one year.

- Management :

- Highly skilled and more competent with these sectors.

- Founder and chairman, both have Tycon of the share market. They have good capabilities to make the profit. Also they have a good track record to generate profits with honesty.

- CEO- he is also a very competent person and serving this company for the last 16 years. Before, I was a market researcher in HUL.

- They have SOPS for daily work, their employees and vendors.

- I have seen CSR activity and I also checked they are spending 2% profits of average 3 years net profit. As per mention in the annual report.

- Promoters have 75 % Shareholding.

- Expansion :

- Working on many projects such as new store openings, Find new market potential, E-commerce and fresh deals.

- Also they are trying to take land for lease instead of buying full properties. This will help to reduce time and cost to open a new store.

- But the lease years must be more than 9 years .It may be 30 years like this. Many landlords offer 9 year leases but they are refusing. This is a good strategy.

- Fresh stores have already started in Mumbai. Anyone can buy online and he will get very near to pick his delivery. This pick up point will be a small shop like 200 -300 sq. feet space with 2-3 people will be available for customer service. Started on pilot basis.

- They are working to make delivery same day or next day .The customers who purchase from online.

- Also have a minimum purchase limit for delivery 1000 SR compared to big basket 1500 SR.

- Risk Factors:

Low Price- Their main motto is to sell at low price as compared to others. But how long they will survive if other players come and also sell at a low price. Then how you hold the customer.

E-Commerce- This market is going to next booms in groceries retailing. Many retailers are already working and many are coming. They are also in the initial stage. How to manage.

6. Subsidiaries:

- Align Retail Trades Private Limited – Company incorporated on 22nd September, 2006, is engaged in the business of packing and selling of grocery products, spices, dry fruits, etc. Its revenue from operations for FY 2019 stood at ` 920.10 crore against `701.86 crore in the previous.

- AVENUE FOOD PLAZA PRIVATE LIMITED (AFPPL):

Company incorporated on 8th June, 2004. It is engaged in the business of operating food stalls at DMart stores. The Company reported net profit after tax of `5.67 crore against `4.17 crore for the previous year.

- AVENUE E-COMMERCE LIMITED (AEL)

Company incorporated on 11th November, 2014 is engaged in the business of online grocery retail under the brand name “DMart Ready”. its mobile app DMart online grocery shopping and through the website www.dmart.in. Customers can either self-pick up their online orders from any designated Dmart Ready Pick-Up Points or get them delivered at their doorstep. The Company registered a loss of `50.82 crore against the loss of ` 48.08 crore in FY 2018.

- NAHAR SETH & JOGANI DEVELOPERS PRIVATE LIMITED (NSJDPL):

Company incorporated on 21st February, 2014, with main object of, among others, development of land and construction and earned net profit after tax of `0.47 crore for FY 2019 against `0.48 crore lakhs for FY 2018.

- REFLECT WHOLESALE AND RETAIL PRIVATE LIMITED (RWRPL)

- Company incorporated on 28th May, 2018, to carry on the business of wholesale and retail of goods and products. It is yet to commence its operations.

Now in Details:

About Management:

- Founder: Mr. Radhakrishnan Damani.

According to Forbes’ Real-Time Billionaires Index, the promoters of D Mart, Mr. Radhakishan Damani, have been named as 2nd richest Indian as on February 15, 2020 with a net worth a $17.8 billion.

- -He is an independent non-executive director of Aptech Ltd..

- He also holds membership in BST ltd, a capital market company in Mumbai which has been active for more than 100 years.

- RD – wear a white shirt and white trousers. That’s why people call him Mr. White.

- The Damani family’s holding in the recently-listed Avenue Supermarts is close to Rs 40,000 crore. It would be “safe and conservative” – as one market watcher puts it, to add another Rs 15,000 crore as the value of RD’s other stock market investments. This is counting out a few more thousands of crores Damani would have made in his stock trading career spanning over 40 years.

- But nobody really knew RD in the 80s. A few people who knew him, called him ‘GS’, because of his ‘entry badge.

- “RD is a very positive player in times of crisis… He’s a shrewd investor; makes more money when he’s bearish,”

- RD was not very active in the market between 2001 and 2004 as he was busy setting up Avenue Supermarts in Mumbai and Gujarat. Several acquaintances have seen RD travelling in his Fiat Uno across Mumbai assessing good spots for his DMart stores. Some people say, RD used to work 12 – 14 hours every day of the week.

- Read more at:

https://economictimes.indiatimes.com/small-biz/entrepreneurship/radhakishan-damani-his-journey-from-dalal-street-punter-to-long-term-investor-to-entrepreneur/articleshow/58230305.cms?utm_source=contentofinterest&utm_medium=text&utm_campaign=cppst

About Chairman: Mr. Ramesh Damani

Currently, Ramesh Shrichand Damani occupies the position of Chairman of Avenue Supermarts Ltd. Mr. Damani is also on the board of Aptech Ltd., V.I.P. Industries Ltd. and Ramesh S Damani Finance Pvt Ltd.

He was a member of Bombay Stock Exchange (BSE) and considered as one of the most successful investors in India. A proponent of the Warren Buffett style of value investing.

He received an MBA from California State University-Northridge and an undergraduate degree from H.R. College of Commerce & Economics.

- Ramesh’s father is the main reason behind Ramesh decision to join the stock market field. Even though Damani is a successful stock marketer, initially, he lost 10000 US dollars in the stock market. Failure is the skipping stone to success, to be noticed.

Massage from Chairman:

Annual Report- 2017:

Our business model has stood the test of time, and we are focused on doing a few things but doing it well and ensuring we continue to be amongst the preferred retailers in India.

- Value retail is a tough business. There is intense competition, and a constantly evolving dynamic in the form of market forces and consumer preferences.

- For nearly 15 years, we have focused on the core needs of our customers, aligned our systems & processes in line with their needs, and delivered steady growth in our revenues and profitability.

Annual Report-2018:

- In the past decade, the retail industry has seen significant changes globally. This is aided by momentum in technology adoption and urbanization.

- In India, nearly half of the country’s private consumption is attributed to the retail industry. With supportive legislation and increasing disposable income, formal retail is expected to see good growth in the coming years.

- Our team has continued directing all efforts towards providing good quality everyday use products at low prices to our customers. We constantly focus on the “voice of the customer” and I believe this has helped us fine-tune our offerings in line with what our customers are seeking.

- We consider our employees, our partners, the society and the environment as important stakeholders of the business.

- Our team has continued directing all efforts towards providing good quality everyday use products at low prices to our customers.

Annual Report-2019:

- Our unwavering focus to delight and surprise our customers has paid off over the years and we are continuing to build on the customer trust we have earned.

- We carry forward our ‘Everyday Low Cost, Everyday Low Price’ model to attract more customers to the world of DMart. We continue to open new stores using our cluster-based expansion model.

- Our employees are central to our operations. Every day, they work hard with the end objective of delivering good quality products at a great value for every customer. They enable DMart to be the customer-centric organisation that we position ourselves as.

- We will continue on our journey to be more accessible and affordable for our customers, by expanding our reach and improving our processes constantly. We strongly value and thank all our vendors and partners for their continued commitment and support. We will always act as a responsible citizen, accountable to society and the environment. Through all this, we will continue to deliver superior shareholder value as well.

2- Managing Director & CEO: Ignatius Navil Noronha.

- He received an undergraduate degree from SIES College of Commerce & Economics and a graduate degree from Narsee Monjee Institute of Management Studies.

- D-Mart was set up in 2001 and Noronha joined it in 2004 as head of business.

- Damani hired Noronha, who was in his early 20s then, from consumer goods giant Hindustan Unilever, where he was a young executive in market research, sales and modern trade.

- People who know him say the recent IPO was the only time when Noronha addressed the media. “He attends conferences and seminars as a participant and not as a speaker,” says an executive who knows him.

- “What makes him special is that he knows how to run the company profitably in a segment that has high overheads,” says the executive with DMart.

- D-Mart owns most of its stores unlike other chains. It is a consistently profitable retailer and has the best margins in the industry.

- Noronha is behind the best practices that have helped DMart, which pays its suppliers within 48 hours of delivery. They, in turn, allow an additional 2-3% gross margin to the chain, enabling it to keep prices low.

- https://www.business-standard.com/article/companies/navil-noronha-meet-the-low-profile-chief-executive-officer-at-d-mart-117032200349_1.html

- India’s richest CEO: Avenue Supermarts’ Ignatius Navil Noronha has net worth of Rs 3,128cr

- HDFC Bank Managing Director Aditya Puri was second on the list of wealthiest non-promoter professionals, with a net worth of Rs 943 crore.

- The third on the list was Ramakant Baheti, Chief Financial Officer (CFO) – Avenue Supermarts, with a net worth of Rs 666 crore.

- CP Gurnani, Chief Executive Officer (CEO) – Tech Mahindra, ranked fourth on the list with a net worth of Rs 594 crore, the report said

CONCALL:

CEO – June 12, 2019

- We should have store level profitability, do not worry about store addition, do not worry about growth, everything will.

- They are working on Fresh and cash and carry models.

- Fresh already started in Mumbai, We now have 196 D-Mart Ready Pick-up Points in Mumbai. They are typical 200-300 square feet stores. On a lighter note, one deep insight is that it is easier to open 200 square feet store compared to 30,000 square

- Earlier we used to say we would purchase real estate but now we are saying we will also do long-term lease because we know, if we want to open more than 20 stores, only ownership will not work but at the same time nine years lease is a very short period for us. So, we are seeing long-term lease. Also, we are working hard on ensuring that our real estate teams are well bolstered.

- We like and hope that everybody in the 3 to 5 Kms radius comes and shops at our stores. That is our simple approach to the business.

- They work on reverse logistic so that reduce the cost of transport.

- We have only one simple principle – if the product is good and business is good, then we will bend our back to ensure that the vendor is comfortable. That is the philosophy.

- We do not want to do what others are trying to do. We want to stand for something a little bit exceptional.

- I come from HUL, I spent eight years there. In fact, I started my career in market research, my first two years was in market research and you can’t believe the kind of work we used to do. So, it’s not easy.

- DIVIDEND NOT PAID WHY? The Company is still in the growth phase. And we have been listed for two years, so our priority at this time is conservation of available money with us and invest the same in growth. And you are seeing growth. So, we believe that is a better deployment of funds, rather than paying back the shareholders. We think the money available with us is better invested in this growth trajectory that we are in.

- The new stores in the same markets reach the absolute high revenue immediately, within three months, six months or one year.

- We now have 196 D-Mart Ready Pick-up Points in Mumbai. They are typical 200-300 square feet stores. On a lighter note, one deep insight is that it is easier to open 200 square feet store compared to 30,000 square

Massage from CEO:

Annual Report- 2017:

- Our first DMart store opened in 2002, our 10th store in 2008, our 100th store in 2016 and we are now at 131 stores.

- As I reflect on the past at each of these milestones, one singular thought that comes to my mind repeatedly is that tomorrow has larger opportunities and newer challenges than today’s achievements. A lot has been achieved and yet, there is so much more to be done.

- The magnanimity and scale of this opportunity continues to keep us awake at night. My team and I are fully aware of this and are striving to build the DMart for tomorrow.

- Year-after-year, we have stayed on the path of providing value through good products at great value, in a functional and convenient environment.

- Our challenge and opportunity is to retain the same level of commitment and relevance among our employees, suppliers and partners to ensure we remain rooted to our core philosophy of value retailing.

- We strongly believe that spending disproportionate time and efforts to up-skill and enhance competencies of existing employees brings significant tangible and intangible long-term benefits to the organization.

- As we garner more footfalls to our stores, we look to further build scale and thus benefit from the resulting economics. Through our ‘Everyday Low Cost / Every Day Low Price’ strategy, we envisage a win-win situation for the customers and the Company

Annual Report-2018:

- The year 2017-18 marked the opening of our 150th store. A significant milestone indeed! It took us 14 years to reach our 100th store and the next 50 opened in 2 years.

- We will continue with our long-standing ethos of “ability having precedence over opportunity.

- We aspire to remain competitive in a challenging and an ever-changing retail environment, while maintaining our value proposition to customers.

- We will remain true to our credo of “Everyday Low Cost /Everyday Low Price” by focussing on achieving higher volumes and keeping procurement and operation costs low thus enabling us to consistently provide good quality products at low prices.

- Our CSR initiatives have made good progress in providing better quality education in public schools of Mumbai. This year our efforts had a positive impact on more than 75,000 school children of the Municipal Corporation of Greater Mumbai (MCGM), by contributing to better infrastructure and learning systems. The direction is aligned towards the same ethos as our business – address each issue as deep and as comprehensively as possible.

Annual Report-2019:

- We follow a cluster-based expansion approach. We thus focus on deepening our penetration in the areas where we are already present, before expanding to newer regions. Using this strategy, we added 21 stores in FY 2018-19, thus ending the year with 176 stores spread across 11 states and 1 Union Territory.

- Our journey to build something valuable, exciting and endearing continued in the year 2018-19, albeit a bit slower. We ended the year with 176 stores, adding 21 new stores.

- We could have done better. While all operating metrics were good, I am personally disappointed with our store opening outcomes. It is partly structural and partly our own weakness. I say structural because we typically prefer to buy land and then construct the buildings.

- I also say it is our weakness because internally there are certain areas in this vertical which we can improve upon. However, it is not a problem we cannot solve, the only question to ask is ‘by when?’ We are working mighty hard on this… we hope to make good progress over the next few years.

- This year operating metrics such as Same Store Sales Growth (SSSG), operating expenditure, turnover per square feet and revenue run rate of newly opened stores was very encouraging. Within those high points, SSSG pleasantly surprised us. It partly compensated for the unsatisfactory new store addition.

- DMart Ready in Mumbai is still very small in terms of revenue as well as scale of operations. In a lot of ways, it is reminiscent of how the DMart business was in the initial days around 15 years back. It took a lot of time. It’s a work in progress.

- We are making a lot of mistakes, but we are learning quickly. We see DMart Ready as a long gestational project that could see relatively significant outcomes after 5-7 years, maybe even more. We are in this for the long term.

- Ocipals schools of Mumbai this year

Business Overview from Annual Reports:

Business & Operation:

Annual Report-2017:

- During FY 2016-17, India saw some key economic policy developments – Demonetisation of Specified Bank Notes (` 500 and ` 1000) prevailing as on 8th November, 2016 and passage of the Good and Services Tax (GST) and the implementation of the same later on.

- India’s GDP grew by 7.2% in the first half of FY 2016-17 on the back of export recovery and implementation of the 7th Pay Commission recommendations which buoyed consumption in the economy. Inflation stood at 3.89% as of March 2017 in line with RBI’s target of 4%.

- Currently, the food and groceries (F&G) segment constitutes a majority share of the retail market (67%). F&G will continue to be the largest contributor in the retail market even four years hence with a projected share of 66% in 2020.

- 16 Indian states contribute approximately 85% of the total retail spend and are expected to continue having a significant share of the total retail consumption.

- The state of Maharashtra contributes the highest share of around 19% among these leading states. The state is expected to continue to reflect this steady growth. Gujarat is another state that is expected to continue to reflect steady growth.

Annual Report-2018:

- During the financial year 2017-18, India continued to grow on the back of strong economic fundamentals. As per the Ministry of Statistics and Programme Implementation, India’s GDP growth stood at 6.7% for 2017-18.

- Owing to the introduction of the e-way bill, GST collections have improved. Monthly GST collections have crossed ` 1 trillion.

- Globally, India is seen as one of the key consumer markets with consumption expenditure set to increase to USD 2 trillion by 2020 and will surpass the consumption expenditure of several other developed economies.

Key factors that will continue to drive this momentum are

- (i) favorable demographics.

- (ii) rapidly rising education levels.

- (iii) steady growth of urbanization.

- (iv) increasing penetration of mobile technology and internet infrastructure

- (v) increasing aspirations and affordability and

- (vi) Government’s focus on reforms, skill development, job creation, infrastructure, manufacturing and investments.

- Organised retail will be a key beneficiary of this rise in consumption. The industry is expected to grow at a CAGR of ~20% to USD 115 bn by 2020, forming 12% of the total retail market

- Food and Grocery will continue to dominate the retail market contributing 66% of the total value in 2020. Apparel & accessories and home & living are the other two key categories which account for 8% and 4% of the total retail market, respectively. Thus, the market opportunity is significantly large for all organized retail operators in India.

- As of 31st March, 2018, we had 155 stores with Retail Business Area of 4.94 million sq.ft., located in Maharashtra (62 stores), Gujarat (30), Karnataka (12), Telangana (19), Andhra Pradesh (10), Madhya Pradesh (6), Chhattisgarh (3), NCR (1), Daman (1), Tamil Nadu (3) Rajasthan (5) and Punjab (3).

Annual Report-2019:

- Your Company delivered yet another year of steady growth by opening 21 (Twenty-one) new stores, thereby taking the total count to 176 stores across the country.

- The Company continued to focus on its existing strategy of offering value retailing to the customers using the EDLC/EDLP (Everyday Low Cost/Everyday Low Price) principle.

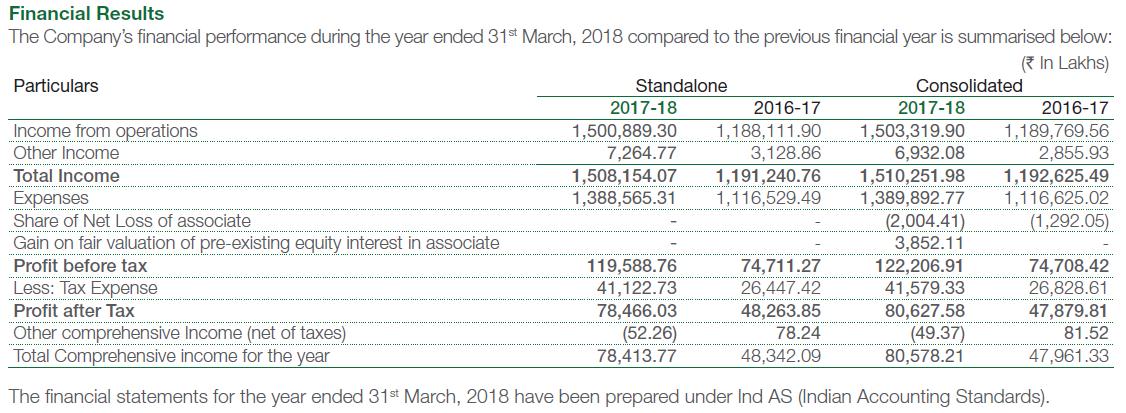

- On a standalone basis, the total income for FY19 was `19,967.66 crore, which is 32.40% higher over the previous year’s income of `15,081.53 crore. Our total income on consolidated basis for FY19 was ` 20,052.87 crore as against ` 15,102.52 crore during FY 2018.

- On a standalone basis, the net profit after tax (PAT) for FY19 stood at ` 936.35 crore as against previous year’s net profit of `784.68 crore thereby recording a growth of 19.33%. Our net profit after tax (PAT) on a consolidated basis for FY19 amounted for `902.46 crore as compared to `806.28 crore in the previous year.

Key Performance Indicators:

Annual Report-2017

- At the end of the Fiscals 2017, 2016, 2015 and 2014, we had 131,110, 89 and 75 stores with Retail Business Area of 4.06 million sq. ft., 3.33 million sq. ft., 2.66 million sq. ft. and 2.14 million sq. ft., respectively.

- We operate distribution centres and packing centres, which form the backbone of our supply chain to support our retail store network.

- As of 31st March, 2017, we had 23 distribution centres and 5 packing centres in Maharashtra, Gujarat, Telangana and Karnataka.

- We have witnessed a steady growth in our total number of bill cuts. Our total number of bill cuts, was 10.85 crores during the fiscal 2017 as compared to 8.47 crores during fiscal 2016.

- Our annualised revenue from sales per retail business area sq. ft. (# ) was ` 31,120 for fiscal 2017 and ` 28,136 for fiscal 2016.

- The IPO of 62,541,806 Equity Shares was offered to investors at a price of ` 299 per share aggregating to ` 1,870 crores.

Share Capital :

- The paid up Equity Share Capital as on 31st March, 2017 amounted to ` 62,408.45 Lakhs.

Dividend:

- With a view to conserve resources and expansion of business, your Directors have thought it prudent not to recommend any dividend for the financial year under review.

Key Managerial Personnel:

- There were no changes in the Key Managerial Personnel during the year.

Employee Salary: Average percentage increase made in the salaries of Employees other than the managerial personnel in the financial year was 12% whereas the increase in the managerial remuneration was 2.31%. The increases in remuneration are as per the policy of the Company.

Annual Report-2018:

- At the end of the Fiscals 2018, 2017, 2016, 2015 and 2014, we had 155, 131, 110, 89 and 75 stores with Retail Business Area of 4.94 million sq. ft., 4.06 million sq. ft., 3.33 million sq. ft., 2.66 million sq. ft. and 2.14 million sq. ft., respectively.

- We operate distribution centers and packing centers, which form the backbone of our supply chain to support our retail store network. As of 31st March, 2018, we had 24 distribution centers and 6 packing centers in Maharashtra, Gujarat, Telangana and Karnataka.

- We have witnessed a steady growth in our total number of bill cuts. Our total number of bill cuts was 13.44 crores during the fiscal 2018 as compared to 10.85 crores during fiscal 2017.

- Our annualized revenue from sales per retail business area sq. ft. (#) was ` 32,719 for fiscal 2018 and ` 31,120 for fiscal 2017

Share Capital :

- The paid up Equity Share Capital as on 31st March, 2018 amounted to ` 62,408.45 Lakhs.

- The Company has neither issued any shares with differential rights as to dividend, voting or otherwise nor issued any sweat equity shares during the year under review.

Dividend:

- With a view to conserve resources for expansion of business, your Directors have thought it prudent not to recommend any dividend for the financial year under review.

Transfer to Reserves:

- The Company has not transferred any amount of profit to the reserves during the financial year under review.

Key Managerial Personnel:

- There were no changes in the Key Managerial Personnel of the Company during the year under review.

CSR Activity:

- In case the Company has failed to spend the 2% of the average net profit of the last three financial years or any part thereof, the Company shall provide the reasons for not spending the amount in its Board Report.

Employee Salary:

- Average percentage increase made in the salaries of Employees other than the managerial personnel in the financial year was 11% whereas the increase in the managerial remuneration for executive directors was 23.87%. The increases in remuneration are as per the policy of the Company.

Annual Report-2019:

- At the end of FY 2018-19, FY 2017-18, FY 2016-17, FY 2015-16 and FY 2014-15, we had 176, 155, 131, 110 and 89 stores with retail business area of 5.9 million sq. ft., 4.9 million sq. ft., 4.1 million sq. ft., 3.3 million sq. ft. and 2.7 million sq. ft., respectively

- We operate distribution centres and packing centres, which form the backbone of our supply chain to support our retail store network. As of 31st March, 2019, we had 35 distribution centres and 7 packing centres in Maharashtra, Gujarat, Telangana, Karnataka and Madhya Pradesh.

- We have witnessed a steady growth in our total number of bill cuts. Our total number of bill cuts was 17.2 crores during the FY 2018-19 as compared to 13.4 crores during FY 2017-18.

- Our annualised revenue from sales per retail business area sq. ft. (#) was ` 35,647 for FY 2018-19 and ` 32,719 for FY 2017-18.

Share Capital:

- During FY 2019 there was no change in the authorized and paid-up share capital of the Company. The paid up Equity Share Capital as on 31st March, 2019 amounted to ` 624.08 crore.

- The Company has neither issued any shares with differential rights as to dividend, voting or otherwise nor issued any sweat equity shares during the year under review.

Dividend:

- With a view to conserve resources for expansion of business, your Directors have thought it prudent not to recommend any dividend for the financial year under review.

Transfer to Reserves:

- The Company has not transferred any amount of profit to the reserves during the financial year under review.

Key Managerial Personnel:

- There were no changes in the Key Managerial Personnel of the Company during the year under review.

CSR Activity:

- In case the Company has failed to spend the 2% of the average net profit of the last three financial years or any part thereof, the Company shall provide the reasons for not spending the amount in its Board Report.

- 3- Years average profit is 819.9 cr. As per promised they have to spend 2% of average 3 years profits around 16.4 cr. They spend 16.55 cr.

- In the financial year 2018-19, through this initiative, the Company has impacted more than 95,000 students from 296 schools.

Employee Salary:

- Average percentage increase made in the salaries of Employees other than the managerial personnel in the financial year was 11.17% whereas the increase in the managerial remuneration was 2.18%. The increases in remuneration are as per the policy of the Company

SUBSIDIARIES:

REPORT ON PERFORMANCE OF SUBSIDIARIES, ASSOCIATES AND JOINT VENTURE COMPANIES:

The Company has 5 subsidiaries as on 31st March, 2019.

- ALIGN RETAIL TRADES PRIVATE LIMITED (ARTPL)

- ARTPL, a wholly-owned subsidiary Company incorporated on 22nd September, 2006, is engaged in the business of packing and selling of grocery products, spices, dry fruits, etc. Its revenue from operations for FY 2019 stood at ` 920.10 crore against `701.86 crore in the previous year and the Company posted net profit after tax of `10.10 crore for FY 2019 against `5.68 crore for FY 2018.

- AVENUE FOOD PLAZA PRIVATE LIMITED (AFPPL):

- AFPPL is a wholly-owned subsidiary Company incorporated on 8th June, 2004. It is engaged in the business of operating food stalls at DMart stores. The revenue from operations of the Company for FY 2019 stood at `23.59 crore as against `17.81 crore for FY 2018. The Company reported net profit after tax of `5.67 crore against `4.17 crore for the previous year.

- AVENUE E-COMMERCE LIMITED (AEL)

- AEL, a subsidiary Company incorporated on 11th November, 2014 is engaged in the business of online grocery retail under the brand name “DMart Ready”. AEL currently operates its business in select areas of Mumbai region. AEL allows its customers to order a broad range of grocery and household products through its mobile app DMart online grocery shopping and through the website www.dmart.in. Customers can either self-pick up their online orders from any designated Dmart Ready Pick-Up Points or get them delivered at their doorstep. AEL’s revenue from operations for FY 2019 stood at `143.59 crore vis-a-vis `44.13 crore in the FY 2018. The Company registered a loss of `50.82 crore against the loss of ` 48.08 crore in FY 2018.

- NAHAR SETH & JOGANI DEVELOPERS PRIVATE LIMITED (NSJDPL):

- NSJDPL is a subsidiary Company incorporated on 21st February, 2014, with main objective of, among others, development of land and construction. Revenue from operations of the Company for FY 2019 and FY 2018 was `0.75 crore and earned net profit after tax of `0.47 crore for FY 2019 against `0.48 crore lakhs for FY 2018.

- REFLECT WHOLESALE AND RETAIL PRIVATE LIMITED (RWRPL)

- A wholly-owned subsidiary Company incorporated on 28th May, 2018, to carry on the business of wholesale and retail of goods and products. It is yet to commence its operations.

- The Company does not have any Joint Venture or Associate Company within the meaning of Section 2(6) of the Companies Act, 2013. No material change has taken place in the nature of business of the subsidiaries.

Competitive Study:

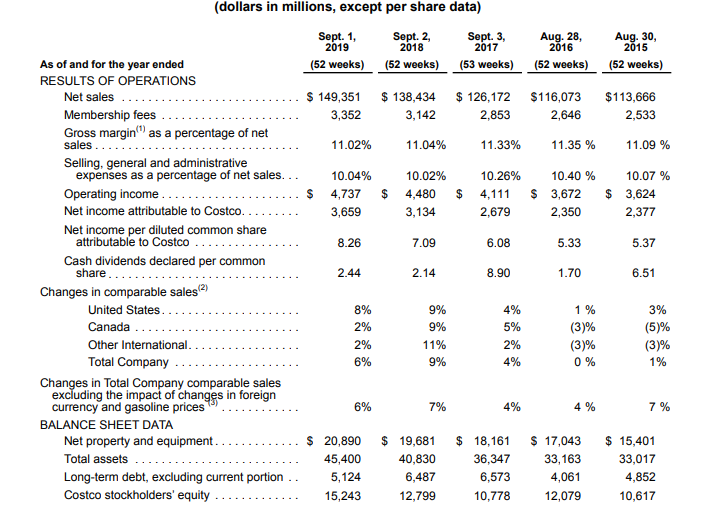

- Walmart Financial Result:

- COSTCO Financial Results:

Add Comment